The Debt Traps of Illegal Online Lenders

Ilustrasi

The number of illegal financial technology (fintech) companies offering loans to the public has increased rapidly. With a promise of ease, they have attracted a large number of borrowers, who can easily fall into their debt traps.

JAKARTA, KOMPAS — In the past two years, a large number of fintech companies have illegally provided online lending services. Through lending apps or websites, the illegal lending platforms offer paperless and hassle-free money lending services.

The target is people who lack financial knowledge and those who are desperate for money to meet their consumptive lifestyles. Various modes are applied to ensnare prospective customers so that those who are not careful enough could get trapped.

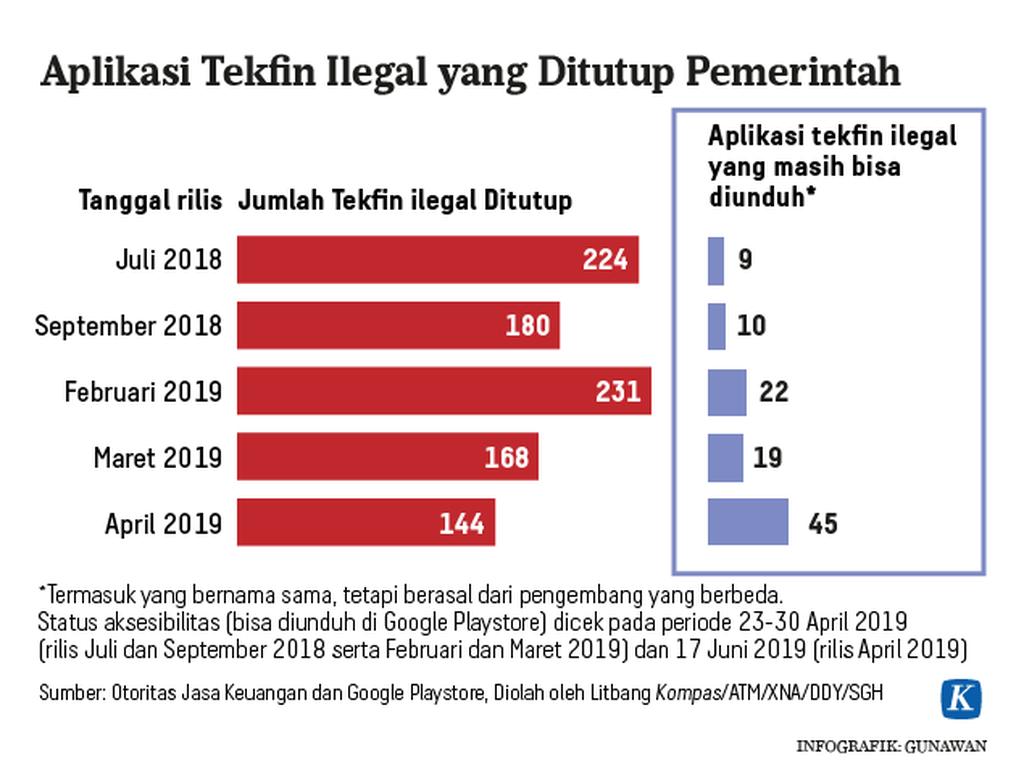

From January 2018 to April 2019, the Financial Services Authority\'s (OJK) Investment Alert Task Force has blocked 947 unlicensed online lending platforms, which are called peer-to-peer (P2P) lending companies.

A fintech company is illegal if does not operate in accordance with OJK Regulation No. 77/2016 on information technology-based lending and borrowing services. According to the regulation, a fintech company should obtain a permit from the OJK to provide lending services to the public.

The fintech firm should meet a number of requirements to obtain a permit. They, for example, must provide a deed of their company establishment, a list of shareholders, data of shareholders and data of directors and commissioners. Although more than a 1,000 of illegal lending applications have been blocked, many illegal lending platforms still operate.

The Illegal online lending platforms aggressively promote their services via text message or social media. They offer minimal requirements in their promotion, which also include their website links.

Without a face-to-face meeting, and with an easy process, the online lenders can provide loans in just a matter of hours. However, behind this convenience, borrowers face big risks such as falling into the debt trap and facing an intimidation.

The information obtained from a number of illegal online loan applications traced by Kompas shows that they mostly charge a lending interest rate of between 1 and 2 percent per day,

between 30 and 60 percent a month. In comparison, the highest interest rate charged by the registered online lending platforms is 0.8 percent a day, or 1 percent a month or 12 percent a year charged by banks.

Intimidation

The promises of easy money have attracted many borrowers. At the end, they fall into the debt trap. They find it hard to obtain the money to finance loan principals, interest payment and late penalties. They also often experience intimidation and sexual harassment from the debt collectors.

FY, 30, a Depok resident, is among customers illegal online lending platforms. FY was tempted to borrow money because the lending requirement was quite easy to fulfill. FY only needed to fill out the form and upload a photo of himself and a photo of his ID card. In less than five minutes, the Rp 600,000 loan was transferred to his bank account. FY applied more loans from other illegal online lending platforms. FY was intimidated, humiliated in front of his friends and sexually harassed because he could not pay the loans.

It is not known exactly how many illegal lending applications are still operating. Due to the large number of victims, the Jakarta Legal Aid Institute (LBH) issued a complaint center in November 2018.

Until the beginning of March 2019 there were 3,091 residents who reported they were victims of the illegal lending platforms or applications. Vloan was one of the illegal lending applications that was closed. The employees were arrested for allegedly being involved in a pornography case. The lending application had tens of thousands of customers. Another fintech application, DT, has been downloaded by 50,000 people.

The office of PT Cash Express Indonesia, which developed illegal financial technology application Angel Cash. At the office, there is no name plate that shows the identity of the company.

The chairman of the Indonesian Consumers Foundation. Tulus Abadi, reminded that many residents had become the victims of the illegal online lenders due to lack of financial literacy. It was indicated by their inability to calculate the amount of interest payments, estimate the maturity period and debt repayment plan.

"They were lured by the convenience being promised. Only by pushing the button of their mobile phones, they can receive the cash. They did not think about the interest payment and how to pay them,” Tulus said.

Personal data

One of the methods of intimidating customers is to use the customer\'s personal data. The telephone numbers of colleagues, bosses, family and relatives can be tracked. In addition, the illegal lenders can also make money from the personal data of their customers by selling them to other parties.

Not surprisingly, the fintech companies rely on the personal data of the customers in running their business. They can collect the personal as soon as the customers download their application and register.

The debt transactions can be carried out through applications if the customers allow the online lending platform to access all their personal data on cell phones. IS ,31, a former debt collector at an illegal fintch company Vloan, said the application used by the company he worked for was able to access personal data from the borrower\'s cell phone.

The fintech company can access the customers’ contact list, photo gallery, short message history, to the history of incoming and outgoing telephones. The company also stored the images of the ID cards and their photos uploaded by the borrows when submitting the loan requirements.

Therefore, IS, which is now a defendant\'s status, acknowledges that the company actually did not really expect the borrowers to repay their debt arrears, including interest and late payment penalties.

Together with three other Vloan employees, IS was arrested for his alleged involvement in the use of pornographic materialsin their efforts to collect debts from borrowers.

A resident shows an SMS message offering an online loan in Jakarta, Sunday (16/6/2019).

An, 24, a former credit analyst at the illegal fintech company, said the failure rate of the debt repayment at his company had reached 50 percent. This condition shows that illegal fintech companies operate not only to profit from their lending services but also from the borrowers’ personal data.

According to An, the customer\'s personal data was offered to other fintech companies such as e-commerce platforms, and big data companies.

Ruby Alamsyah, a digital forensic practitioner, said that the illegal online lending applications used masking techniques. It means there are two applications combined into one. The site shows only an application related to lending, while the other application which a feature enabling it to access the data on the borrower\'s mobile phones is not seen.

"Here, there is a gray area legally. On the one hand, taking personal data without permission is a crime because it is regulated in the ITE Law. But, on the other hand, the borrowers are unaware that they have allowed the use of their data when downloading the app," Ruby said.

The chairman of the OJK’s Investment Alert Task Force, Tongam L Tobing, said that the online lending platforms were allowed only to collect the photos, voices and addresses of the customers during the process of submitting the loan application. Accessing customer contacts is very unjustified and vulnerable to abuse, he added.

"There is a possibility that the illegal fintech companies use the data from the contact data they access for financial gains," Tongam said.

OJK director for licensing and supervision, Hendrikus Passagi, acknowledged, the stealing of the personal data in the digital industry has become a common practice. For this reason, the people must be very careful when using online services. The public must ensure that their data does not change hands to other parties and are misused. (BKY/IGA/ILO)